What can go wrong will go wrong - Algostable Trouble

What can go wrong will go wrong - Algostable Trouble

On why Terra foundered, the economic designs of stablecoins and the imminent regulatory siege.

There is a TL:DR at the end of the post.

A Terrable moment for crypto

On May 10, 2022, TerraUSD (UST), an algorithmic stablecoin, started to lose its peg against the U.S. dollar and dropped all the way to $0.6. Its pair token, LUNA, tanked more than 50% in less than 24 hours. At the time of writing, UST is worth roughly 1.5 cents and Luna is worth nearly zero. The Terra 2.0 revival plan was activated, which created a forked chain without UST. The old chain was subsequently renamed Terra Classic (LUNC).

This is, in fact, a Lehman moment for crypto as a top 10 market cap coin once worth more than $40 billion was wiped out in a matter of days. Murphy’s law, which states that “What can go wrong will go wrong” serves the crypto market a cold reminder that something that’s too good to be true is probably not true.

The faults in the design of algo-stablecoin have been belabored by many. The death spiral situation that Luna-skeptics previously anticipated was displayed in its naked form like a step-by-step playbook. Here is a recap of how UST is supposed to maintain its peg1:

UST and Luna are sister tokens that all live on the Terra blockchain.

The rules of the game, powered by smart contracts, are that traders should always be able to exchange $1 worth of Luna for $1 of UST.

If UST dips below $1, traders can “burn” UST (remove it from circulation) in exchange for $1 worth of Luna, which will reduce the supply of UST and raises its price.

If UST is above $1, traders can burn Luna and create new UST, which increases the supply of the stablecoin and pushes the price back toward $1.

Analogies for Terra’s model, which points to the inevitability of its collapse, are plenty. In some way, the system operates like a perpetual motion machine. But soon people realize that such thing is impossible and in fact, the machine is manually cranked by hand (i.e. the huge funds raised to subsidize Anchor Protocol’s yield).

The system is also like a house of cards because the only thing holding it together is "confidence”. When market is ebullient and liquidity is abundant, no one worries about the fundamentals of the system. This is, at the same time, the very fault of the mechanism as it requires people to believe they won’t be the unlucky one to be stuck holding their bag. Once the “confidence” dissipates, the structure caves due to the lack of backstop to defend and restore the faith. Here is an excerpt from Matt Levine to hone in on the point:

“The basic thing that makes Terra valuable is confidence in it. The essential source of this confidence is ... just sort of recursive social belief? If you think that everyone else will treat Terra as worth a dollar, then you will treat it as worth a dollar, and you won’t sell it for $0.90 in a panic, which means that it won’t go down to $0.90, etc. But if you think that everyone else will treat Terra as worth zero, then you will dump it as fast as you can at whatever price you can get, which means that it will go down below $0.90, etc.”

Here are a few links if you want to read more about the details the collapse:

On Economic Design of Stablecoins

Warning signs about algo-stablecoins’ design, specifically on Terra’s model, were not absent. Research by the now-defunct Diem Association was published a while back in August 2021. The paper primarily discusses two crucial dimensions that underpin the economic design of every stablecoin:

the volatility of the reserve assets against the reference asset, which defines the risk profile of the stablecoin for coin holders; and

the degree to which the stablecoin is exposed to the risk of a death spiral

The authors concluded that although decentralized stablecoin designs eliminate the need to trust an intermediary, they are either exposed to death spirals or highly capital inefficient, as they must be highly over-collateralized to account for the lack of an intermediary. Essentially, the so-called algorithmic stablecoins should really be called “under-collateralized stables”.

Another key thought experiment to evaluate the risk of stablecoin is how safely can the stablecoin wind-down. That is, how safely can the supply of the stablecoin goes to zero. For a sufficiently collateralized stablecoin, it should be able to maintain its peg until the very last unit of supply.

Terra’s design fails this test. Looking at the figure above, the authors categorize stablecoin that’s “Fully backed in protocols’ own investment token” as the most likely candidate to suffer death spiral risk. It is in fact, impossible for UST to safely unwind back to zero supply. This is because UST is backed by its endogenous token (LUNA). As UST’s supply decreases, the investment token supply expands, which increases downward pressure on token price. The reserve’s value would then quickly fall to zero in the absence of a backstop.

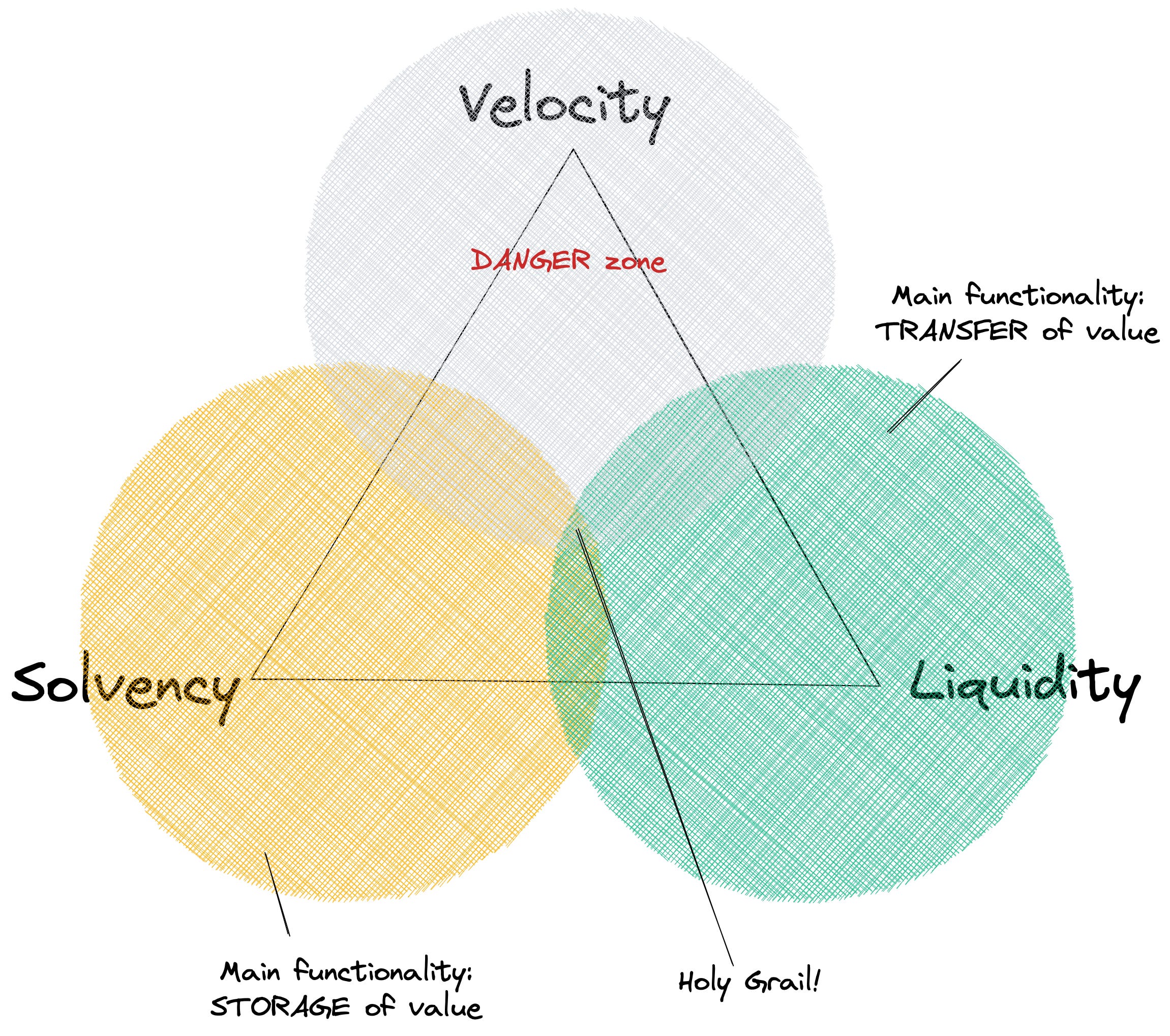

The crypto world loves a good "trilemma”… blockchain trilemma, bridge trilemma, privacy trilemma… you name it. So here is another one — stablecoin trilemma. Luca Prosperi, who writes Dirt Roads, puts forward the below criteria in evaluating stablecoin designs:

Velocity: how easy it is for a stable to scale up

Solvency: how reliable is the value backing the currency — i.e. its peg

Liquidity: how robust is the peg against short-term shocks

Terra, which prioritizes velocity, falls under the Danger Zone in this model. In order to blitz scale UST, Terra’s design allows the protocol to print new money without injecting exogenous collateral into the system. This in turn sacrifices solvency and liquidity and eventually causes Terra to founder. Simply put, Terra’s (or Do Kwon’s) ego is writing checks that its body can’t cash.

Apart from the trilemma model, we can also take a look at the major risk events that algo-stables face and appraise their coping mechanisms:

Sudden Price Drop (of investment token) - pair token going down >30%

Speculative Attack - continuous sell pressure on the algo-stable and investment token

The arbitrage mechanism in Terra’s design could address moderate de-pegging events given that the overall confidence of the system is unfazed. However, in the event of a sudden price swing and speculative attack, a well-collateralized reserve fund is required to act as a backstop and restore faith amidst a confidence collapse. At its core, algo-stables are not that different from sovereign currencies that peg to the US dollar, such as the HK dollar. Just take a look at the explanation from HKMA on the Linked Exchange Rate System (LERS):

Of course, one major difference between a sovereign currency and an algo-stable is the ubiquitous adoption of HKD as a medium of exchange, store of value, and unit of account within the jurisdiction of the city’s territory. The government makes it illegal to not accept its own currency as a medium of exchange and requires tax payments in its own currency. These are the real-world use cases that algo-stables simply cannot replicate just by incorporating the coin into more DeFi protocols and “expanding its utility”. Nonetheless, even a sovereign currency has to rely on collateral/reserve funds to fend off ravenous peg attackers. During the Asian Financial Crisis, George Soros infamously attempted to attack the weak end of the HKD. In the end, the HKMA’s $US82 billion in reserves at the time proved enough to keep the peg at 1:7.8.

There is blood in the water

While the collapse of Terra wrecked havoc across the crypto market, caused mass liquidations and sharp drops in DeFi TVL, its effects were largely contained within crypto. This is due to the fact that UST’s use cases are rather limited in the real world with little traction as a medium of exchange.

Most of UST were deposited into Anchor Protocol, which is a DeFi savings protocol promising a lucrative 20% annual yield. Some have argued that it is precisely the limited real-world adoption and Anchor’s unsustainable yields that led to Terra’s collapse. Were UST given more time to expand and entrench itself deeper to the payment systems, its widespread adoption could prevent a total confidence collapse and a death spiral. As Arthur Hayes puts it in a recent blog:

The death spiral is no joke. This is a complete confidence game. It’s a confidence game akin to the current debt-based fractional banking system; however, this game does not have governments who can coerce usage of the system with the threat of mortal violence.

Nonetheless, a contrary argument could be made that UST’s collapse in its relatively early stage is a fortunate misfortune. Were UST more intertwined with the broader financial system, the disastrous consequences of a de-pegging event would be unthinkable. In a world where UST was widely adopted as a means of payment and store of value, a drop in the UST’s value would have colossal spillovers to traditional financial markets.

Crypto market is in fact bleeding, and the smell of blood has attracted the sharks. Days after Terra’s downfall, US Treasury Secretary Janet Yellen doubled down on her stance that stablecoins pose a threat to financial stability during the annual testimony before the Senate Banking Committee. She also stressed that Congress should be working on stablecoin legislation, saying that it is “highly appropriate” that this gets done by the end of 2022.

In the UK, Rishi Sunak, the Chancellor of Exchequer, said that “Legislation to regulate stablecoins, where used as a means of payment, will be part of the Financial Services and Markets Bill.” The department said it would include plans to regulate stablecoins as a payment mechanism in financial legislation. Meanwhile, some are not happy to see opportunistic regulators seizing the bully pulpit. Jake Chervinsky, the Head of Policy at the Blockchain Association, puts it bluntly:

“I don't know who needs to hear this but it's generally a bad idea to put people in charge of regulating things they don't understand 1/100th as well as twitter anons“.

The bottom line is that increased regulatory scrutiny can be expected and future legislation may establish legitimacy and encourage adoption for centralized stablecoin instead of decentralized one.

Stablecoin’s potential impact on banking

Though peg stability is the top concern for stablecoin, it is not the only concern. Regulators rightly take a much broader perspective and also look at the consequences of the proliferation of centralized stablecoin. This is quite fair given USDT slightly de-pegged to $0.96 in early May amid the market turmoil caused by Terra.

Research published by the Fed at the end of last year authored by Gordon Liao and John Caramichael looked into stablecoin’s potential impact on the traditional banking sector, specifically on its effect on commercial banks’ ability for credit intermediation. Here the Fed’s anticipating a scenario where stablecoins get so big that people would switch cash and bank deposits for it. Such a situation may challenge the fundamental mechanisms of credit provision and money creation2.

The authors present three plausible centralized stablecoin reserve frameworks: narrow bank, two-tiered intermediation, and security holdings:

Narrow bank - stablecoin is a liability of the central bank but accessed by households and firm (roughly equivalent to a retail CBDC).

Two-tiered intermediation - stablecoins would be backed by commercial bank deposits and used for fractional reserve banking.

Cash-equivalent securities - stablecoin issuers would hold treasury bills and high-quality commercial paper instead of bank deposits.

Below are the author’s findings and conclusions:

Narrow bank

can lead to disintermediation of traditional banking, but may provide the most stable peg.

Two-tiered system

can both support stablecoin issuance and maintain traditional forms of credit creation.

Securities Holdings

stablecoins backed by adequately safe and liquid collateral can potentially serve as a digital safe haven currency during periods of crypto market distress.

What we can infer is that centralized stablecoin will likely be regulated similar to banks going forward. And that’s not necessarily a bad thing! This is because a bank-like regulatory framework would imply applying the “two-tiered intermediation” approach for stablecoin issuers, which is most unlikely to cause credit disintermediation and poses the smallest risk to the existing fractional-reserve banking system3. Since the report was published, here are some of the news headlines:

Stablecoin firms should be regulated like the banks they are (Feb 12, 2022)

Treasury official: Regulate stablecoin issuers like banks to avoid 'cleaning something up later' (Apr 9, 2022)

Morgan Stanley Says US Could Regulate Stablecoin Issuers Like Banks (Apr 22, 2022)

Time to get serious about self-regulation

In response to the expected heavy intervention from regulators, Ryan Selkis, founder of Messari, quite rightly calls for industry self-regulation. His main propositions include:

Align on a pro-user "crypto pledge" from policymakers

Crowdsource a Digital Asset User Bill of Rights

Enact common-sense consumer protections

Regarding stablecoin, Selkis specifically mentioned the creation of standards around Proof-of-Reserves and Proof-of-Collateral:

“This seems like a non-negotiable at this point. Exchanges and custodians that support stablecoins should demand proofs of reserves and collateral behind the assets they list. That doesn’t mean that each supported asset will require a 1:1 reserve or overcollateralization rate necessarily, but it does mean that collateral and credit-worthiness gets listed right alongside APY…. This won’t be a choice within a matter of months. Best to make the investment proactively today, and notch the goodwill win while we can.”

Whether self-regulation is good enough to appease regulators is unclear. Nevertheless, it is a starting point to cleanse crypto’s bad reputation as “scammy” and “full of frauds”. Terra’s collapse, though painful, serves as a healthy jab to the crypto market that will hopefully prevent a future crisis.

TL;DR

Terra’s collapse is a result of a “confidence collapse”, since recursive social belief is what propelled its growth in the first place.

Arbitrage mechanism alone unable to defend the peg under market stress, algo-stablecoins require additional reserves to prevent death spirals.

A safe decentralized stablecoin should be able to wind down its supply to zero without breaking the peg.

Regulations are imminent and might establish legitimacy and boost the adoption of centralized stablecoin.

Centralized stablecoin issuers could affect commercial banks’ role in credit intermediation depending on reserve regulatory framework.

Crypto industry self-regulation, specifically on stablecoin’s proof of reserve, is being called for to appease regulators.

This is tied to the concept that the majority of money in the modern economy is created by commercial banks making loans. For more details, you can refer to this report from the Bank of England. The basic idea is that banks do not really first take the deposits from people and then lend them out. Rather, banks create money and deposits through lending [Quite a tricky and counterintuitive concept that may deserve a future post].

Of course, some may argue that fractional reserve banking system itself carries many faults. This relates to a much broader debate on full-reserve vs. fractional-reserve banking, which I will not go into here. There is a lengthy transcript of a House Hearing on this topic back in 2012 if you have a lot of time.